The economic landscape is fraught with uncertainty making forecasting 2012 very difficult. U.S. GDP figures for the first (Q1) and second quarters (Q2) of 2011 were revised down and barely remained in positive territory.

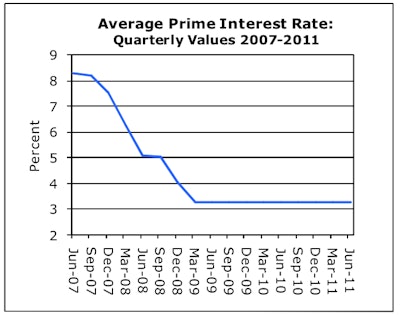

In September the Federal Reserve announced a new plan to shift from short- to long-term bonds in the hope of driving down interest rates further to spur the housing market.

Global stock markets reacted negatively for two major reasons: one, the move will flatten the so-called yield curve and make it harder for businesses such as insurance companies to make adequate returns on their portfolios; two, and maybe the most important factor, is the Fed’s statement that it was “acting because it saw little prospect that the economy would expand fast enough and soon enough to help the 25 million Americans unable to find full-time work.”

Unemployment has been above 9% for many months. The Fed went on to say, “there was a significant risk that ‘strains in global financial markets’ could further damage prospects for recovery.” The statement has been interpreted as an indication that the Fed is worried about the economy slipping into a double dip recession.

The 2011 construction equipment market rebounded strongly compared with 2010. It appears that a large part of the growth was due to inventory replenishment.

Inventories at manufacturers peaked in the third quarter (Q3) of 2008 and declined by approximately 30% by Q1 of 2010. As of Q2, 2011 inventories are almost back to the pre-recession level.

No one knows what field inventories are at construction equipment dealers. Statements from manufacturers are that by Q1 of 2010 the “cupboard was bare” with virtually no inventories of finished machines. The strong rebound of retail sales has been fueled in part by inventory rebuilding. Unfilled orders, an indication of the strength of backlogs, are at a high level as well, providing manufacturers with encouragement to increase production rates throughout the year.

I originally forecasted that 2011 would be up about 14% compared with 2010. It now appears the market will be up 32.6%, more than twice my original estimate. The rapid increase in demand in 2011 was termed by some as a “bull-whip” effect. However, it is not likely to extend the same level of gains in 2012 unless consumers get back to consuming.

Consumers represent two-thirds of our economy. So far the recovery has been led by one-third of the economy, the manufacturing sector, largely due to strong export markets.

Throughout 2011 a great deal of the U.S. construction machinery demand came from equipment users who had projects ahead of them and replaced existing machines on a one-for-one basis (no fleet expansion), and from mining markets, especially coal, iron, copper, and oil and gas development, especially shale oil in states where that type of activity is unusual such as in Pennsylvania, South Dakota and Colorado. Demand was lacking from owner-operators (individuals who own one or two machines).

The primary leading indicator for construction equipment demand has always been housing starts, which have been flat-lined at an annualized rate of just over 500,000 units since the beginning of 2009.

Seeking the “new normal”

2012 will be a challenging year for equipment manufacturers. I believe we’ll see strength in machinery markets that serve the mining market. The rigid hauler market, which is primarily a mining market, is expected to be up more than 36%.

Articulated haulers will also benefit from the mining boom, especially in smaller coal mines in the Eastern U.S. and in the Alberta oil sands.

Products that are important to the housing market such as skid steer loaders and rubber-tracked loaders will benefit from the slight improvement in that market. A large percentage of telescopic handlers are used in apartment construction, which is booming right now. The multi-family segment of the housing market now represents 30% of all unit starts.

The crane market, which is a late cycle market, will probably recover in 2012 with the market up about 13%.

Manufacturer and dealer inventories will be replenished by January 2012. Unless Federal legislators begin to cooperate, it is likely we will see negative GDP growth in Q1 of 2012. That’s not a double dip. A full recession is defined as two consecutive quarters having negative GDP growth.

Housing starts are expected to increase, but only slightly, maybe up to 750,000 units on an annualized basis. The Federally Funded Highway Bill will probably be funded, but to what level is unknown. I believe that in 2012 we will be searching for a new level of normal. Overall, I’d forecast that machine sales will be up about 9.1%.