How do the off-road and on-road markets compare from the point of view of suppliers of components or powertrains? There are many differences you need to be aware of in order to address this market. Some of the key variations are detailed below.

Off-Road Is More Open to Hybrids

Within the on-road market, hybrids are yesterday’s news. Full electric is the future. Hybrids have fewer incentives from regulators and few (if any) major OEMs are investing significant sums of money in new products. It would be a slight exaggeration to say that hybrids in trucks and buses are dead. Hybrid vehicles will continue to be produced, but only in small numbers.

Off-road it is a different story, however, with full electrification of larger machinery posing a major challenge. Due to the duty cycles, it’s difficult to complete many hours per day at high power with a fully electric vehicle, as the battery will run out of energy. In addition, the weight of the battery is also a consideration. Subsidies and government support offered for full electrification of trucks and buses have largely not been rolled out to off-highway. Finally, off-road machines are often more complicated. In addition to the main motor/engine, there are separate systems required for work functions and hydraulics, which all serves to make hybrid systems worth considering.

However, this may change. It’s not difficult to imagine the same dynamics that played out in on-road eventually leading to reduced interest in hybrids and more full electrification, although this is not on the horizon presently for larger machinery/vehicles.

Off-Road May Have a Wider Range of Powertrain Solutions

In trucks and buses, use of other fuels such as hydrogen, methanol and hydrotreated vegetable oil (HVO) is not as widespread a topic of discussion than it is in the off-road market. That isn’t to say these fuels won’t be used, but it seems highly likely if they are it will be in lower volumes, as they generally won’t compete well with full electrification after factors such as cost, infrastructure and environmental expectations are taken into consideration.

Given the demanding duty cycle for electrification, the off-highway sector needs to consider other options. Net-zero climate targets make it likely diesels won’t be around for forever. Therefore, companies are looking seriously at other alternatives for off-road machines. Which of these solutions comes to the forefront remains to be seen and, after considering infrastructure, fuel availability and cost, it can be argued none will have a strong competitive position against diesel until it is banned, limited by regulation, or more heavily taxed.

The slow pace of electrification in off-road doesn’t mean suppliers should avoid this market though, as volume will come later and those that invest early are likely to emerge the winners.

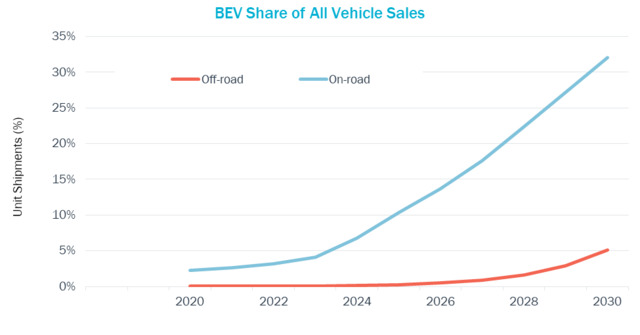

Meanwhile, electrification of smaller off-road machines is flourishing. Forklifts were already 64% electric in 2022 (including a small amount with fuel cells), scissor lifts were 89%, and boom lifts 25%. Largely as a result of this, 1.5 million or 27% of off-highway vehicles/machines covered by this report were already electric in 2022. However, if we exclude these categories, fully electric vehicles did not even reach 0.1% in off-road during 2022, with 2027 forecast to be just under 1% and 2030 about 5%. This is a much slower pace of growth than the truck and bus market.

The graph below compares on-road (trucks of 6 tonnes+ and buses) with off-road (all categories included in our research except forklifts, scissors and boom). The 3% rate of on-road electrification achieved in 2021 is forecast to be reached in off-road in 2029.

Electrification of most off-road machines will lag far behind that of trucks and busesInteract Analysis

Electrification of most off-road machines will lag far behind that of trucks and busesInteract Analysis

Off-Road Has More Variety

A component for one truck can be used in another because the powertrain of a distribution truck is very similar to a long-haul truck of a given size, for example. If required, you could use exactly the same or a very similar powertrain for both. Powertrains for intercity buses/coaches are also similar to urban buses.

Off-road, with about 6 million vehicles sold in 2022, is similar in market sizes to trucks and buses (if we include pickup trucks and vans, then trucks is much bigger), but the variety is much greater. In our research reports we cover tractors, wheel loaders, backhoe loaders, skidsteer/crawler loaders, bulldozers, aerial work platforms, tractors, combines, telehandlers, hauler-dump trucks, and others, each with very different usage requirements and powertrain designs. None of the powertrain components used in a small, hand-operated forklift could be reused in a large excavator.

In on-road you can create one product and then sell the same, or similar, product in volume. In off-highway a separate design is required for each vehicle type, and even for different customers, while offsetting lower volumes against anticipated higher profit margins.

Off-Road Is a Tougher Environment

Off-road environments include mines, construction sites and farms, which tend to involve more dust and dirt. It can also be noisy, terrain can be less smooth, and the range of speed and acceleration requirements may be higher. All this has to be factored into the design of a powertrain and selection of components. Sometimes this means little change to existing on-road products, or simply a protective cover. More often, a completely different design or even fully customized products are required.

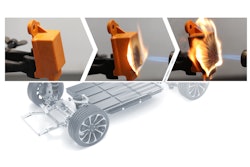

Dust and dirt is thought to be a particular concern for fuel cell systems, which makes their adoption in off-road more challenging. While the fuel cell doesn’t need to be fundamentally different, it needs better protection from the environment and more regular changing of filters.

Off-Road Components Cost More (on a $/kW or $/kWh basis)

Gathering prices for both off-road and on-road has helped me refine the data by cross-checking them against each other. However, in many cases, significant differences in prices between the sectors make perfect sense.

Unlike the truck market, you cannot produce one motor and then reuse it in many different types of off-highway equipment due to the vastly different duty cycles, and power and torque requirements, as well as very different sizes of machine. This — combined with the lower volumes in off-highway — means motors and inverters are, on average, 46% more expensive in off-road per kW, according to our data.

Our research indicates battery packs in off-highway vehicles are 41% more expensive per kWh than on-road (medium and heavy-duty trucks and buses). Cell costs remain similar, but packaging requires more work due to differences in level of robustness, space and reliability. The same modules cannot be reused in many cases and prices vary substantially. The battery price for forklifts, which in some cases can use lead acid batteries, and have higher volume and commoditization, is even lower than trucks. In extreme cases, such as a very large, specialized machine for mining, where only a handful of units will be produced, the battery pack price per kWh could be more than double the on-road case.

Almost all of the extra cost in an off-road electrified powertrain comes from the battery pack. Fuel cell costs are only slightly higher (due to volume), as are onboard chargers, and DC-DC converters are often less expensive in off-highway, due to the smaller voltage range.

Off-Road Has Less Competition for Components

It is rare to see a component company specializing only in off-road. Most companies focus on both, or only on-road (for now). For on-road in recent years, we have been told of tough competition on pricing as many companies bid for the same quote. In off-road, this is less common. If anything, there seems a need for more suppliers to enter the market to help drive innovation and price reductions.

In Off-Road, Battery Pack Revenue Share Is Lower

In 2022, the battery pack accounted for more than half the on-road dollars, compared with only 38% in off-road. This is an empirical finding, but we think the reasons could be the need for higher peak power (in some cases meaning more expensive motors and inverters) and a lack of range anxiety. In off-road, you are very often near your company so less margin for error is required in the battery pack.

Differences in Component Architecture

E-axles remain a hot topic for trucks, but not in off-road, perhaps due to different shapes and architecture of off-highway vehicles. Less need for aerodynamic shapes may also be a factor in how components are packaged.

The type of motor is more mixed off-road. On-road, the permanent market dominates, with a little over 90% of units and revenue. However, our data shows off-road induction and synchronous reluctance have a larger role to play.

James Fox is principal analyst at Interact Analysis.