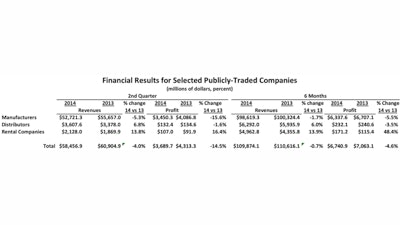

Manfredi & Associates has compiled the financial results of many publicly traded companies associated with construction and mining equipment to get a gauge on how the market fared in the second quarter of 2014. Overall, revenues were down 4% and profits were down 14.5%. The industry was divided into three groups: manufacturers, distributors and rental companies. There were major performance differences among the three groups. Manufacturers reported second quarter 2014 revenues down 5.3% with profits down 15.6%. Distributors reported second quarter revenues up 6.8% but profits were down 1.6%. Rental companies are outperforming the other segments with second quarter revenues up 13.8% and profits up 16.4%. It appears that organizations closest to their customers perform better than others involved in the industry.

Individual company results are displayed below. Companies deeply involved in agriculture such as AGCO and Deere reported down revenues: -9.8% and -8.9%, respectively. Their performance is not surprising given the fact that year-to-date U.S. sales of agricultural tractors 100 hp or more are down 8.7%, four-wheel drive agricultural tractor sales are down 11% and combine sales are down 15.2%.

The mining equipment sector has been particularly hard hit. Joy Global reported its second quarter revenues were down 31.7%. The drop in mining also affected Caterpillar. It managed to eek out a profit gain of 4.1% despite a revenue decline of 3.2%, which was largely caused by a 28.5% drop in the revenues of its resource industries segment that supplies equipment to the mining industry. AB Volvo also reported second quarter revenues were down 8.7%. The Volvo revenue figure is for all their operations including trucks and engines. The company’s construction equipment segment reported a second quarter 2014 revenue decline of 7.4% that was largely due to a 29.7% decline in the company’s Asia market region.

The equipment distributor segment fared somewhat better than the manufacturers with revenues up 6.8%, but profits down by 1.6%. Readers should note that with the exception of Titan, all of the distributors in the analysis are based in Canada because most U.S. distributors are not public companies and data is not available. The Canadian companies are benefiting from a good economy, especially in the oil sands region in Alberta. It should also be noted that, Finning, based in Vancouver, British Columbia, with Canadian operations in BC and Alberta, is the largest Caterpillar dealer in the world and has operations in the U.K. and Ireland, as well as the southern cone of South America. Finning benefitted from the robust Canadian economy as well as renewed economic growth in the U.K. Gains in both regions have been tempered by declines in the company’s South American region that is almost entirely mining related.

The equipment rental segment is once again the star performer with a second quarter 2014 revenue gain of 13.8% and a profit improvement of 16.4%. This group is benefitting from the industry trend toward renting more and owning less. The performance metrics of this group are extremely positive. Hertz was kept in this table despite the fact the company has not yet reported its second quarter 2014 results and is in the process of restating its results for the past several years. There is no word yet on when the restated results are expected.

Manfredi & Associates believes that the 2014 market will yield considerable improvements. Growth will be back-loaded to the second half. The company expects the mining sector bloodletting to slow in the second half of 2014 on the theory that it can’t get much worse. Mineral commodity prices are still at levels that should encourage equipment investments. The U.S. coal industry is still under siege from the EPA that is issuing increasingly restrictive generating plant regulations, making upgrading and investing in coal-fired plants very risky. The U.S. housing market is well on its way to exceed one million housing starts, a recent milestone for this important construction segment. Housing construction drives a great deal of other construction activities and will benefit equipment sales. The extension of the Federal Highway Trust Fund will allow for the continuation of projects underway and pending. Non-residential construction is on track to grow between 10 and 15% this year, which means the second half of the year will be very robust. Energy related projects such as fracking and wind farm construction will be strong for the balance of the year.

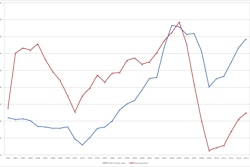

There is no better source for tracking retail sales of construction equipment than the manufacturers themselves. Both Caterpillar and Komatsu publish data that tracks retails. Caterpillar’s is based on a survey of its dealers. The data is a three month moving average of the percent change year-over-year for its regions. That means the data has been smoothed. Komatsu publishes the monthly percent change in its retails for each of its regions. A graph of each series appears below.

To make the two data series comparable, the Komatsu data has been converted into a three month moving average in order to compare the retail results with Caterpillar’s results. They are remarkably similar. Together they portray a picture of a North American retail trend that is encouraging. The percent change in retail sales of construction equipment turned up for both companies in August 2013 and has continued on a mostly positive track since then.

Manfredi & Associates believes there will continue to be an improving sales pattern for the balance of 2014 and probably well into 2015, and is sticking with the forecast made last year when we predicted 2014 U.S. retails would be up between 5 and 10% compared with 2013.

2015 Forecast

The U.S. economy has been limping along for several years. U.S. Gross Domestic Product (GDP), the broadest measure of economic activity, has been growing since 2009, but just barely. The table below illustrates that the $17 trillion economy has been steadily growing.

However, examining the percent change from quarter to quarter the pattern is not a steady upward trend. This recent up and down economic pattern with no strong surge forward is one reason the Federal Reserve is keeping interest rates low and continues to express concern about the future.

Total construction as measured by the U.S. Department of Commerce has finally recovered. The number of dollars put-in-place reached bottom in 2011 and has been increasing since then. Total construction will reach $1 trillion in 2015, or approximately 6% of the total economy. In the early 2000s the construction industry represented nearly 10% of the total economy

The source of funding has changed over this time period. In past downturns Federal and State governments have jumped in and funded construction projects in order to bolster economic activity. This time around the major spending has been from the private sector not the public sector. The percent of construction funded by the private sector is expected to climb to more than 70% in 2014 and will probably be slightly less than 75% in 2015.

The improving sales pattern, at least for the first half of 2015, will be advanced by increases in housing starts. Housing is the engine that propels the economy in general and construction machinery sales in particular. Single family starts dropped dramatically when the great recession began and has been very slow to return to normal levels. In the 1990s and early 2000s starts were averaging 1.5 million units per year. One and a half million units was considered by most economists adequate to house new immigrants, provide for new family formations and replace dilapidated housing. The graph that follows illustrates the current situation. The figures are annualized data plotted monthly. Monthly annualized starts have been trending slightly below one million annual units for several years, which is an unacceptable level. At the end of the recession multi-family starts exceeded single family starts, which is very unusual, as people displaced from their homes because of financial trouble struggled to find adequate housing. Total starts were underperforming compared with previous historic periods because of a shift to multifamily and because so many people, especially young people who were unable to find jobs, moved back home with their parents.

Single family housing is an important driver of demand for construction machinery. Building single family structures is much more equipment-intensive than multi-family construction.

Road building is the mainstay of the construction equipment industry. For one thing the activity is noticeable to everyone. A person can’t drive anywhere in the country without encountering men working or work zone notices. Funding for this activity is largely from government sources - state, local and of course Federal. Most people believe that Federal funding has been inadequate to keep up with the country's dilapidated infrastructure. Spending for roads has been erratic as illustrated in the following graph. The horizontal line represents the spending trend over the past five and a half years: almost exactly horizontal, which means there has been no change during the entire period. Annual spending is approximately $82 billion per year.

Energy production, especially shale gas, has gotten a lot of attention in the past few years. It is proving to be a boon to the U.S. economy and has the potential to allow the U.S. to become energy independent. Production development is unusual because it affects areas of the country where equipment demand is traditionally slow, or almost non-existent. The following map illustrates the major discoveries. Currently, the most active areas are in North Dakota, the Bakken deposit, and in western New York and Pennsylvania in the Marcellus and Utica deposits. Demand for equipment in these areas is at an all time high. Overall, shale gas production is up more than 500%.

Construction employment is a strong indicator of equipment demand. Employment is expected to reach six million people in 2014 and expected to reach 6.5 million people in 2015. The 2015 level is still far below the slightly less than 8 million people who where employed in construction in the 2006/2007 period. The lower level compared with 2006/2007 is due to shortages of skilled workers. The Associated General Contractors (AGC) has been complaining for the past year about the lack of skilled workers and the constraint that shortage is putting on construction activity.

The labor shortage is helping to grow the equipment rental business more rapidly than overall construction. Contractors will be spending more on renting equipment as they attempt to take on more and more work with fewer people while keeping their capital costs to a minimum. Jobsite automation is propelling the rental business to new highs. Manfredi & Associates forecasts that in 2015 equipment rentals per employee will reach $6,500. It also predicts that construction employment will reach 6.5 million people. Do the math and that implies that total U.S. rental revenues will reach more than $40 billion in 2015. High rental revenue growth is also good for equipment demand because rental companies have become the single largest purchaser of equipment in the U.S.

Manfredi & Associates' total 2014 forecast turned out to be spot on. Overall the year will end with retail sales up 7.3%. There were big gains in sales of wheel loaders, up 10.5%. Track and skid steer loader sales were up slightly less than 10%. Articulated truck sales were up 15.4% due to rental companies replenishing their fleets. The big miss was the crane market which was originally forecasted to be up 12%, but will actually be up 4%, or perhaps less. Rigid hauler retail sales continue to suffer from the slowdown in coal mining particularly in the East.

The 2015 market will grow at slightly less than 12% overall with the largest gain in the skid steer loader market and the tractor loader backhoe market. Both of those markets will benefit from the continued growth of housing starts. Most product markets will end 2015 on a positive note. Exceptions are the crane market and the rigid hauler market, both will decline about 10%.