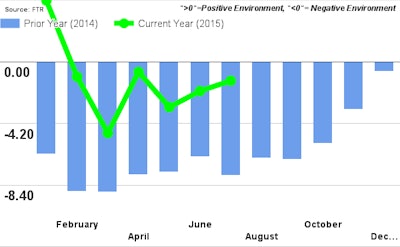

FTR’s Shippers Conditions Index (SCI) for July, at a reading of -1.3, continues to reflect the short-term stability of capacity utilization and steady fuel prices that are aiding shippers in containing costs. However, FTR expects the SCI to fall gradually during the balance of 2015 with a more severe negative downturn in 2016 due to forecasted stronger freight conditions and rising fuel prices.

The SCI is a compilation of factors affecting the shippers transport environment. Any reading below zero indicates a less-than-ideal environment for shippers. Readings below -10 signal that conditions for shippers are approaching critical levels, based on available capacity and expected rates.

Jonathan Starks, Director of Transportation Analysis at FTR, comments, “Shippers continue to operate in an environment in which freight demand is okay, but not great, and capacity is available, but not abundant. The supply and demand equation for trucking has certainly loosened during 2015 but is still operating at historically tight levels. This has enabled carriers to continue their work on raising base rates, while at the same time shippers are still benefitting from the rapid reduction in fuel costs at the end of last year (and occurring to a minor degree right now). So far, the drop in fuel has been enough to overcome the raises in contract rates. That will change once we hit 2016 and the low fuel prices will be reflected in year-over-year comparisons. Truck rate data coming from Truckstop.com highlights that the spot market has softened considerably from last year, with pricing (excluding fuel) down over 6%. This should be a positive for shippers in the near-term since we expect contract pricing to reflect that behavior, and many shippers should see smaller base rate increases during winter negotiations. The big caveat is that the regulatory environment still looms large, although it is looking more like a 2017 phenomenon rather than 2016.”