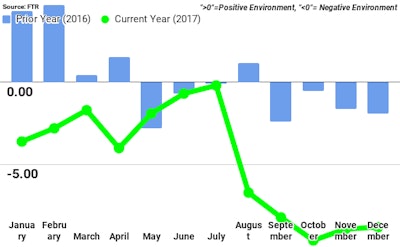

FTR’s Shippers Conditions Index (SCI) for December was basically unchanged from November at a reading of -8.8. Carrier capacity remains extremely tight with rate acceleration expected through Q2, keeping the index in decidedly negative territory through early 2018.

Jonathan Starks, Chief Operating Officer at FTR, comments, “The question for many shippers is how long will the tough times last? When we look at freight demand, which has been strengthening for nearly a year now, our forecast shows robust demand for most of 2018. If there will be improvements for shippers, it won’t be because of a softening of freight. Truckstop.com’s Market Demand Index, at roughly twice the level that it was at this time last year, highlights the tight capacity situation within the spot market. It began rising again in February after softening following the strong holiday season. For shippers who haven’t locked in capacity, this year’s spring shipping season will be a tough one.”

The Shippers Conditions Index could improve later in the year dependent upon how much carriers can add capacity to meet the strong demand, as well as shippers adjusting supply chains to enhance carrier productivity.

Avery Vise, VP of Trucking at FTR, comments, “We are seeing record truck and trailer orders, which indicate buying above replacement demand, and much of that will hit the market in the second half. However, that narrative is somewhat disrupted by ELD implementation and the driver shortage. People naturally think of the driver shortage in terms of the supply of drivers, however, changes in carrier productivity are just as important. We anticipate that shippers and carriers will implement a host of productivity enhancements -- measures like drop-and-hook, better scheduling for pickups and deliveries, faster dock turnarounds, better coordination among shippers through intermediaries, and so on. Higher rates motivate shippers to be much more flexible on steps that increase carrier productivity.”