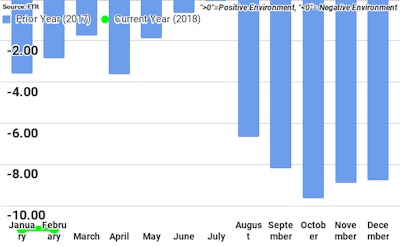

The February Shippers Conditions Index reading from FTR was unchanged from January at -11.1, reflecting an unfavorable environment for shippers. Regulatory pressures are rising, and the capacity required for a hot freight market was slow to increase in the first quarter, putting pressure on rates. Freight growth during the first quarter typically softens after a strong holiday season, but not in 2018. FTR’s truck loadings index is expected to see growth of 4% to 6% year over year into 2019. A continued capacity crunch in the truckload segment could result in bleed-over of freight volume to LTL which would further increase shippers’ costs.

Jonathan Starks, Chief Operating Officer at FTR, comments, “Shippers remain in the throes of a pro-carrier environment. Every major indicator of demand--manufacturing, payroll employment, retail sales, housing construction-- is at least at the strongest level since the Great Recession. Unemployment is at a 17 year low, and the driver shortage continues to create capacity constraints.

“Rates on the spot market continue to remain elevated, and we don’t expect to see any significant downward rate pressure - whether spot or contract - until at least 2019. Shippers should not expect to get near-term relief from spot rates that are at or near record levels. Securing capacity at a reasonably higher price remains the key challenge for shippers.”

Todd Tranausky, Senior Research Analyst at FTR, comments, “Intermodal rates are expected to follow truck rates higher and grow at more than 5% compared with the 2017 period through the balance of the year. The next few months will see rates grow even faster, leaving shippers paying more to move their goods in a tight freight market.”