The current slump in sales of commercial vehicles globally can be found above all in Western Europe, Brazil and China; and overall, the cyclical industry is likely to see a continuation of its descent after its record-breaking performance in recent years. That’s according to the AlixPartners Global Commercial-Vehicle Industry Outlook announced today by AlixPartners, the global business-advisory firm.

In the medium term, says the study, further expansion is valid, especially in newly-industrializing countries where the sales-growth trend for commercial vehicles remains sustainable. However, in the longer term, a mature and thus cost-driven commercial-vehicle market will only provide enough return on investment for those manufacturers that can capitalize on economies of scale, overcome historical inefficiencies and continue their globalization, including by localizing products and supply chains. Moreover, says the study, cost reductions can be achieved through worldwide economies of scale in products and in sourcing, including by adopting modular strategies, and by using optimized processes in cooperation with suppliers.

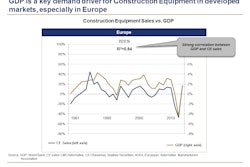

In Europe, notes the study, the euro crisis has triggered a second commercial-vehicle market recession, and has superseded the usual eight-year cycle in the sector. In Western Europe, says AlixPartners, sales this year are expected to decline 15% to 20% vs. last year, with 2008 sales levels probably not being reached until at least 2015.

Meanwhile, recent sales declines in Brazil, says the study, were mainly caused by the introduction of the “Euro V” exhaust standard in that country. And declines in China can be traced back to governmental decrees designed give the market a “breather.”

“Despite the current slump in Europe, Brazil and China, the driving forces for growth globally remain intact,” said Francesco Barosi, managing director at AlixPartners and co-lead of the firm’s global Heavy Equipment Practice. “However, weak revenues regionally show how important an international presence is for commercial-vehicle manufacturers.”

The largest commercial-vehicle manufacturers have at least five reasons to take a vital interest in expansion into developing countries, says the study. First, to take part in the explosive growth in developing markets today. Second, to offset declines in mature markets. Third, to achieve economies of scale on the investment side. Fourth, to achieve economies of scale on the purchasing side. And fifth, to achieve economies of scale in terms of meeting fast-globalizing emissions standards.

“Globalization enables commercial vehicles manufacturers to reach a critical mass,” said John Hoffecker, managing director at AlixPartners and leader of the firm’s global Automotive Practice. “In a cyclical and increasingly mature market, only companies that take full advantage of scale will be able to achieve satisfactory returns on investment.”

Local Vehicles, Global Platforms

However, notes the study, a key part of “going global” is having the right localization model for developing markets. That includes such things as on-site assembly, a network of local suppliers and a distribution and service network. And, because achieving these things from a standing start can take several years, the study predicts that acquisitions, shareholdings, joint ventures and other collaborations with local partners will become the norm in the future.

“We especially expect further consolidation among suppliers in the future,” said Barosi. “With the exception of the large Chinese manufacturers and a few Indian players, local payers are probably too small to be able to successfully resist the competition that’s coming over time.”

Despite rising globalization, big manufacturers still must meet an increasing variety of regional standards and client requirements, says the study. This includes emissions and safety requirements, and differences in things like distances typically travelled by commercial vehicles in various countries.

“In order to meet this high degree of complexity with minimum costs, parts standardization and modular design are necessary,” said Barosi. “The commercial vehicles of the future will be based on common modular strategies for all local and specific sectoral variants, which can be assembled on a ‘variant-flexible’ local assembly line.”

Big Savings to be had in Production and Development

AlixPartners predicts that commercial-vehicle assembly from the chassis through electronics, as well as production processes, will be modularized and standardized worldwide. Evaluations by the firm show that doing so could shave 20% off production costs and 30% off development costs.

The study also predicts that “value” commercial vehicles – those currently being built by local companies in developing countries – will for some time have major cost advantages over “Western” commercial vehicles, even those built in developing countries. Accordingly, Western companies should move to make sure that important modules, such as brakes and axles, will be manufactured by suppliers in developing countries, using a high degree of automation.

“’Value’ vehicles will have an impact on the market in Europe and the U.S. as well,” said Barosi. "It is therefore very important for global manufacturers to drive this development themselves.”

Improved Cooperation with Suppliers

The study also identifies potential cost reductions through greater cooperation with suppliers. A comparison with automotive production shows that the cooperation between commercial- vehicle manufacturers and their suppliers can be improved.

“The potential in this industry with suppliers is far from being exhausted,” said Hoffecker. “In developing countries, vertical integration is still very high. Accordingly, better-leveraged supplier bases in these countries have enormous potential – which could also pay off via the exporting of components to Western countries."

Greater transparency across the value chain, says AlixPartners, could optimize joint planning and the steering of capacities, risks and costs. According to the firm, Tier 1 suppliers are often not ready to take on the responsibility for a complete parts system – but OEMs often also don’t want to “give away” responsibility. The result is double-work, produces changes, delays and cost over-runs.

The study also suggests an improved understanding between manufacturers and suppliers regarding technical changes and production runs, to harmonize deliveries and to achieve joint savings.

Diesel Improvements Remain the Name of the Game

While meeting new emissions and fuel-economy rules are forcing manufacturers to develop new drivetrains, the study predicts that most of the action will be in smaller diesel motors – which, in turn, will employ such features as optimized combustion, superchargers, exhaust-gas recycling and exhaust gas after-treatment. The electrification of commercial vehicles, says the study, will for the time being be reserved only for vehicles in urban areas, and at that mainly buses and light-distribution vehicles.