Sentiment in European farm machinery posted a +5.0 index number for June following +15.0 in May. The results for the last 12 months were +36.2, +30.0, +28.0, +26.0, +20.0, +25.0, +23.0, +26.0, +23.0, +20.0, +15.0, and +5.0. The business climate index (CBI) peaked in February 2018 and then trended lower before stabilizing in the 20s in November 2018. The index dropped below 20.0 in May and the deterioration accelerated this month. Survey participants’ expectations for the United Kingdom have collapsed and this has also been evident in monthly tractor numbers due to Brexit concerns. Confidence for larger markets like Germany continues to weaken, although recent sales have been fairly strong. Changes in business sentiment moving forward will probably depend on countries that continue to have optimism, like France, Spain, Italy, and, to a lesser degree, Austria and Switzerland. On average, the CEMA survey participants still expect an increase by 3% in 2019. Deere and AGCO are guiding the European market to be flat in 2019.

Dealer stocks are at relatively high levels. Incoming orders, both from the EU and from outside the EU, are weakening and a further slowdown is expected. For the tractors and harvesting equipment sector, both the current evaluations and future expectations have declined significantly. A majority of survey participants expect turnover declines from most European markets for the first time since 2016. In the June report, 30% of operators now expect their business to grow within the next 6 months, versus 41% 2 months ago; 28% expect turnover to decrease for the next 6 months, versus 22% 2 months ago. About 75% of participants evaluate current business conditions as very good, good, or satisfying, flat sequentially, down from 83% 2 months ago. The remaining 25% of participants would evaluate their current business conditions as unfavorable to very unfavorable, up from 17% in April.

Regional updates

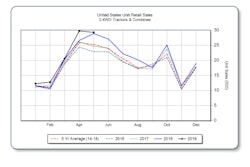

The U.K. deteriorated the most in terms of business climate, and inventories are swelling. U.K. tractors decreased 27% year-over-year in May. Year-to-date, U.K. tractors were down 3%. We believe there was some pull forward of U.K. tractor demand earlier in the year, led by OEMs that wanted to have inventory ahead of continued Brexit concerns. Larger markets like Germany remain on the softer side with regard to confidence. Overall German tractor registrations were up 18% year-over-year in May 2019. Low-horsepower (<100 hp) tractor registrations were up 40%. High-horsepower tractor registrations (100 hp+) were up 4%, with tractors in the above-150 hp category down 4% and the midrange of 100-150 hp was up 23%. Year-to-date, German tractors were up 22% with low-hp up 47% and high-hp up 9%. For Romania, Belgium, and the Netherlands, a majority of participants expect turnover decreases. On the bright side, the positive outlook for France continues to solidify, while Spain, Italy, and Switzerland maintain the positive expectations but have lost some momentum.