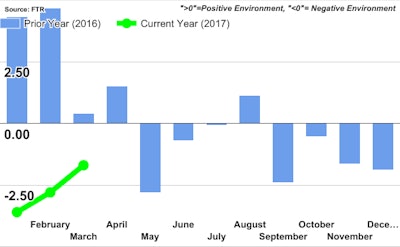

FTR’s Shippers Conditions Index (SCI) for March, at a reading of -1.7, remains in marginally negative territory. Currently, softer freight conditions and a view of adequate capacity over the past 18 months have slowed the expected decline in this index. Any market-wide tightness reflected in recent tightening of spot rates is currently less than originally thought, but there are risks to shippers’ complacency in not being prepared for a crises in capacity availability that still may happen as ELD and other factors affect the market towards year end.

The SCI is a compilation of factors affecting the shippers transport environment. Any reading below zero indicates a less-than-ideal environment for shippers. Readings below -10 signal that conditions for shippers are approaching critical levels, based on available capacity and expected costs.

Jonathan Starks, Chief Operating Officer at FTR, comments, “The trucking market still seems to be in a relative balance with enough available capacity to move goods at reasonable pricing. However, that balance is slowly shifting toward the carriers. Spot market load activity is well above levels we saw last year, and spot pricing has recently hit double-digit increases. This pricing increase is partially due to increases in fuel pricing that occurred back in mid-2016, but it is also stemming from a modest reduction in capacity at the same time that load activity has increased. The potential for significant capacity tightness to occur by late 2017 is increasing as the freight environment is strengthening from a resurgence in manufacturing, construction, and industrial activity. Add in a potential capacity reduction due to the Electronic Logging Device (ELD) implementation in December, and the trucking market is poised for a significant change in 2018.”