New Flyer Industries Inc. (NFI), the largest transit bus and motor coach manufacturer and parts distributor in North America, has announced its financial results for the 13-week period ended April 1, 2018 (2018 Q1). Full unaudited interim condensed financial statements and the Management's Discussion and Analysis (the MD&A) are available at the company's website. Unless otherwise indicated all monetary amounts in this press release are expressed in U.S. dollars.

2018 First Quarter Financial Results

Year-over-year comparisons reported in the MD&A compare 2018 Q1 to the 13-week period ended April 2, 2017 (2017 Q1). Organizational changes to better align business functions within operating segments were made effective January 2, 2017. This organizational change was implemented in two phases. In 2017, over-the-counter parts sales were moved from the coach operations to aftermarket operations. In 2018 the service function, comprised of technical service management and customer training, which was previously managed by the aftermarket operations, of MCI only, was moved to the coach manufacturing operations. To improve the comparability between periods, the related prior year segment information has been restated to reflect these changes.

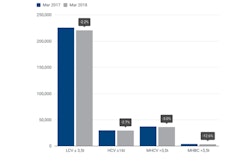

Volume increased as a result of higher transit bus deliveries and the inclusion of ARBOC deliveries offset by a reduction in motor coach deliveries. Motor coach deliveries are seasonal, with comparatively strong fourth and softer first quarters; however 2017 Q1 deliveries were stronger as a result of recovering NewJersey Transit deliveries following the contract deferral in 2016. Additionally, management believes tax changes in the U.S., related to accelerated depreciation, resulted in a seasonably stronger 2017 Q4, followed by a weaker 2018 Q1.

Revenue from manufacturing operations for 2018 Q1 increased by 0.6% compared to 2017 Q1. The increase in 2018 Q1 revenue primarily resulted from a 11.3% increase in new transit bus, coach and cutaway deliveries compared to 2017 Q1 deliveries, as well as the inclusion of the revenue to third parties for the fiberglass reinforced polymer components operations. This increase was offset by a 10.6% decrease in average selling price per EU in 2018 Q1 compared to 2017 Q1. Manufacturing business revenue for 2018 Q1 of $478.6 million is $6.2 million lower when compared to proforma manufacturing business revenue (which includes ARBOC) for 2017 Q1.

The decrease in average selling price is the result of normal volatility, changes in the product sales mix and the inclusion of ARBOC's units which have a substantially lower selling price than the average heavy-duty transit bus or motor coach.

Revenue from aftermarket operations in 2018 Q1 increased by 4.1% compared to 2017 Q1.

Net earnings during 2018 Q1 decreased by $7.5 million compared to 2017 Q1 resulting in a decrease in net earnings per common share (Share) in 2018 Q1 of $0.48, compared to $0.61 per Share in 2017 Q1 primarily as a result of the following events: $3.9 million past service cost adjustment (net of tax) related to a collective bargaining agreement which commenced on April 1, 2018 and a $2.8 million (net of tax) unrealized foreign exchange loss on non-current monetary items. The impact of these events to net earnings per share was $0.11.

Management believes that ROIC is an important ratio and metric that can be used to assess investments against their related earnings and capital utilization. ROIC during the last twelve months ended April 1, 2018 was 15.4%, as compared to 14.6% during the last twelve months ended April 2, 2017 improving primarily as a result of a decreased effective tax rate ("ETR") under the U.S. tax reform effective December 22, 2017, as well as improved net operating profits.

Consolidated Adjusted EBITDA for 2018 Q1 increased by 3.4% compared to 2017 Q1.

The 2018 Q1 manufacturing Adjusted EBITDA increased 11.1% compared to 2017 Q1 primarily as a result of increased deliveries, improved margins and the inclusion of ARBOC's operations. Contributors to the increase in margin included a favourable sales mix and continued cost reductions achieved through the Company's operational excellence initiatives. The pro forma manufacturing business Adjusted EBITDA per EU (which includes ARBOC) for 2018 Q1 was $54,300 which is $2,500 higher per EU when compared to 2017 Q1.

Margins vary significantly due to factors such as pricing, order size, propulsion system, product type and options specified by the customer. Management cautions readers that quarterly Adjusted EBITDA and Adjusted EBITDA per EU can be volatile and should be considered over a period of several quarters.

The 2018 aftermarket operations Adjusted EBITDA decreased by 13.1% compared to 2017 Q1 due to sales mix and costs involved in consolidating the New Flyer and MCI parts business. Aftermarket sales and margins remain difficult to forecast due to a significant portion of the business being transactional in nature, and as a result experiences significant quarterly volatility.

Liquidity

The amount of dividends declared increased by 39.5% in 2018 Q1 as a result of the increase in the annual dividend rate from C$0.95 to C$1.30 per Share effective for dividends declared after May 10, 2017 and additional Shares issued as a result of conversion of NFI's previously outstanding convertible debentures.

The liquidity position of $204.1 million as at April 1, 2018 is comprised of available cash of $15.3 million and $188.8 million available under the revolving portion of the company’s credit facility (Revolver) as compared to a liquidity position of $222.3 million at December 31, 2017. The decrease in liquidity relates to changes in non-cash working capital. Changes in non-cash working capital are primarily a result of seasonality and are expected to be temporary in nature. Management believes that these funds, together with share and debt issuances, other borrowings capacity and the cash generated from the company’s operating activities, will provide the company with sufficient liquidity and capital resources to meet its current financial obligations as they come due, as well as provide funds for its financing requirements, capital expenditures, dividend payments and other operational needs for the foreseeable future.

PPE cash expenditures in 2018 Q1 increased by 84.4% compared to 2017 Q1 primarily as a result of investments in facilities, increased part fabrication capacity at the company's new Shepherdsville, KY, facility and as a result of insourcing and continuous improvement programs.

The company's total leverage ratio (defined as net indebtedness divided by Adjusted EBITDA) of 1.90 at April 1, 2018 increased from the ratio of 1.84 at December 31, 2017. The company is well within compliance with its banking covenant that requiring the total leverage ratio to be less than 3.50.

Outlook

The company’s annual operating plan for the 52-weeks ending December 30, 2018 (Fiscal 2018) is focused on maintaining and growing its leading market position in the heavy-duty transit bus, motor coach and cutaway bus markets and aftermarket parts distribution through enhanced competitiveness.

On March 23, 2018 the U.S. Congress passed the 2018 fiscal year budget which included appropriations for public transportation of $13.5 billion. The American Public Transportation Association (APTA) has recently indicated that the federal budget is a big win for public transportation. According to APTA, the total appropriations of $13.5 billion is the largest amount appropriated for public transportation in an annual spending bill and the largest one-year increase, with more than $1 billion over last year.

Based on an aging fleet, overall economic conditions, expected customer fleet replacement plans, and active or anticipated procurements, management continues to expect procurement activity throughout the U.S. and Canada to remain stable through 2018.

MCI continues to develop and expand its product portfolio. The new D45 CRT LE coach introduced in 2017, with its revolutionary improvements to support people with disabilities, is undergoing testing at the bus testing facility in Altoona, PA, in order to qualify as a vehicle that is eligible for purchase using FTA funding. The new MCI 35 ft. coach, the J3500, is undergoing electronic stability control calibration and certification. Production capability to support the manufacture of these vehicles will be in place in the second half of 2018 with deliveries expected to begin in early 2019.

As the population ages and ease of access becomes more of a focus, management also believes the demand for low-floor cutaway and medium-duty buses with greater accessibility will grow from its current level of 5% of the total cutaway market. The company estimates that ARBOC delivered 64% of all the low-floor cutaway buses in 2017. ARBOC is currently testing its medium-duty bus (Spirit of Equess) at the testing facility in Altoona, PA, and is pleased with customer response anticipating deliveries starting in the second half of 2018.

The company’s master production schedule combined with current backlog and orders anticipated to be awarded by customers under new procurements is expected to enable the company to deliver approximately 4,350 EUs during Fiscal 2018. Production rates are adjusted and can vary from quarter to quarter due to product mix and contract award timing.

With a current healthy production schedule, low leverage, and solid liquidity, management continues to be focused on PPE investment and estimates PPE expenditures for Fiscal 2018 to be in the range of approximately $63 to $73 million. This estimate is approximately $8 million higher than what was originally disclosed, as the revised range includes amounts that were planned for Fiscal 2017, but were carried forward to Fiscal 2018 and also as a result of a better understanding of the PPE investments needed in the newly acquired composite businesses. Spending relates to equipment maintenance as well as growth projects which management expects to generate margin enhancements consistent with its targets.

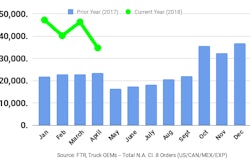

Although part sales remain difficult to forecast, management expects the parts market to remain relatively stable in Fiscal 2018. Management believes the increase in gross orders received of 1.2% in 2018 Q1 as compared to 2017 Q1 is promising but, will be subject to quarter-to-quarter volatility which is typical for this business segment. The company continues to focus on its established customer base to provide best value and support and also continues to investigate incremental business programs such as vendor managed inventory contracts which are anticipated to be at lower margins. The company previously announced it is closing a redundant parts distribution center in Hebron, KY, in July 2018 and continues to assess further opportunities for cost reduction once the New Flyer and MCI Parts businesses are fully harmonized with a common IT system - expected to be completed in the second half of 2018.

Dividends

Based on the improvement in business performance as well as the company's outlook, the company's board of directors (the Board) has approved an increase of 15.4% in the annual dividend rate. The new annual dividend rate of C$1.50 per Share is effective for dividends declared after May 9, 2018. The Board believes that the new dividend rate has been established at a sustainable level, although such distributions are not assured.