The National Fluid Power Association (NFPA) has announced the availability of the latest Global Fluid Power Report and Forecast from Oxford Economics. The winter edition of the forecast details global macroeconomic trends and provides in-depth analysis for the fluid power industry.

Members of NFPA can access the full Global Fluid Power Report and Forecast here.

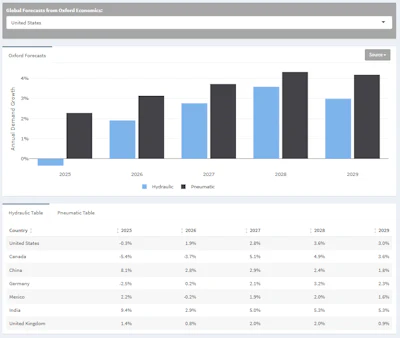

The report includes a global macro summary, by-country customer market forecasts and analysis, and by-country fluid power industry forecasts. It is designed to offer insights for professionals in the fluid power sector.

Analysis is provided for numerous key industrial markets. Countries covered in the report include the United States, Canada, Mexico, Brazil, Germany, Italy, the United Kingdom, China, Japan, India and South Korea. The full report is available for access through the NFPA.

Oxford Economics released the following summary of updates with the latest forecast release:

- Despite global GDP growth ending 2025 on a soft note, we do not expect this weakness to persist. Indeed, we believe that the sluggishness will prove to be temporary, as the drag from weaker domestic demand growth in some major economies and the US government shutdown fades. Hence, we expect momentum to recover as 2026 progresses and forecast that aggregate GDP for the countries in this report will average 2.7% for the year.

- Our 2026 annual aggregate industrial production growth forecast for the countries in this report is 3.1%, down from 3.3% in 2025. However, growth will remain uneven across regions and sectors. In 2025, tariff uncertainty was partly cushioned by front‑loading and implementation lags; as these effects fade, industry enters 2026 with softer momentum.

- Optimism for the US and China does not extend to most other advanced economies. U.S. tariffs are likely to prolong the soft patch in imports, muting spillovers from domestic strength, while China’s export dominance is eroding competitors’ performance weighing on industrial output.